2026 Salary Survey: Navigating change in Canadian construction and design

Sixteen years in, Construction Canada’s annual salary and industry survey continues to tell the story of a sector in motion. Built on the experiences of professionals across the country, this year’s report captures the realities behind the projects shaping Canada’s built environment, from hospitals and office towers to housing and public infrastructure.

As the official publication of Construction Specifications Canada (CSC), the magazine reflects a wide range of perspectives, bringing together specifiers, architects, engineers, contractors, and product specialists. While most respondents are not CSC members, participation from the association dipped slightly this year. Even so, their voices remain a key link to the technical rigour and standards that underpin project success.

The 2026 survey revisits core themes, regional trends, job satisfaction, industry outlook, and workforce demographics, while continuing to track emerging shifts. Artificial intelligence (AI), introduced last year, remains a developing force, with early signs that its influence is beginning to take hold across design and delivery processes.

With more than 100 additional responses compared to 2025, this year’s findings broaden the lens. Together, they reveal an industry navigating uncertainty, yet steadily adjusting—finding its footing between ongoing pressures and a cautious sense of optimism about what comes next.

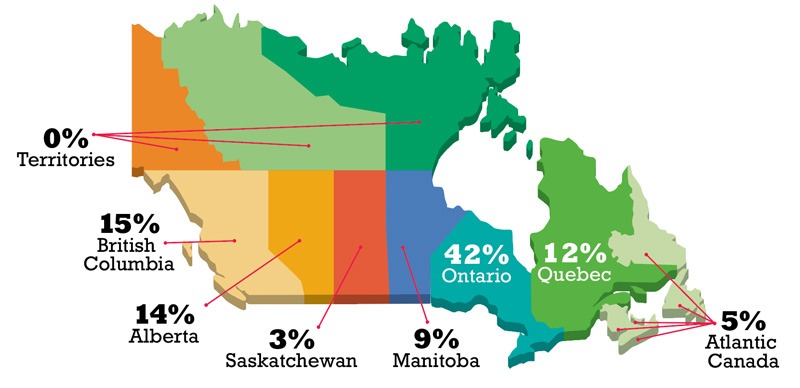

This year’s survey drew responses from across Canada, with all provinces represented but no participation from the territories. Ontario remained the most represented region at 42 per cent. British Columbia and Alberta held second and third place, while Quebec moved closer in fourth, rising by four points. Other regions remained largely stable, maintaining a consistent national view.

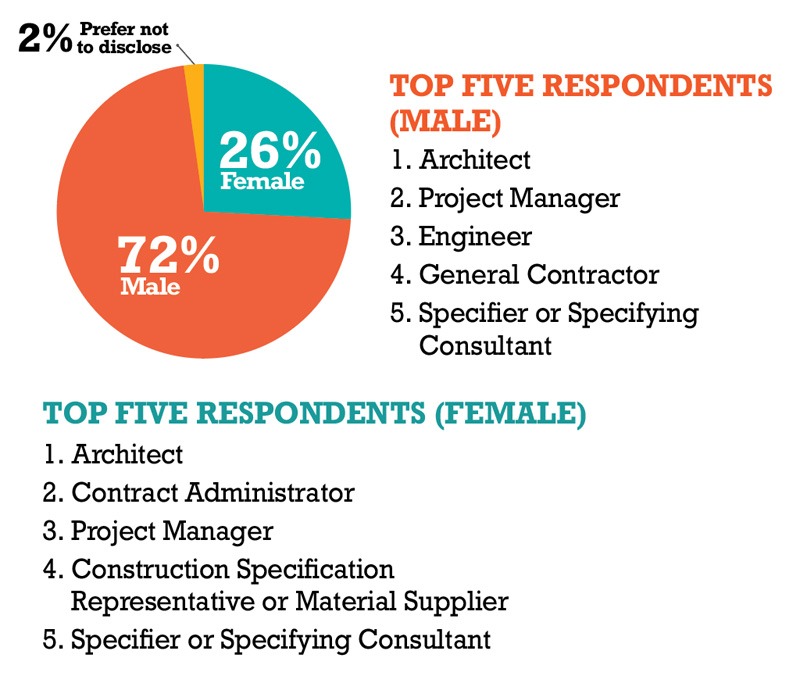

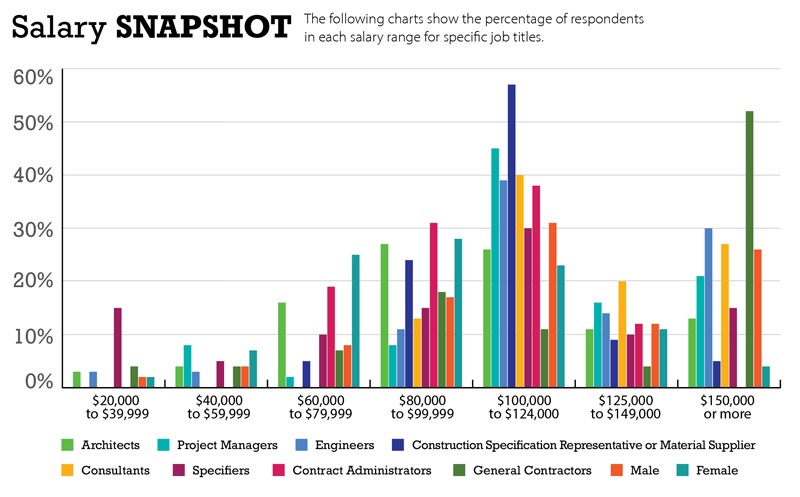

Women accounted for 26 per cent of respondents, unchanged from last year. However, 38 per cent reported earning $100,000 or more, a slight decline. Male respondents held steady, with 69 per cent reporting incomes at or above that level.

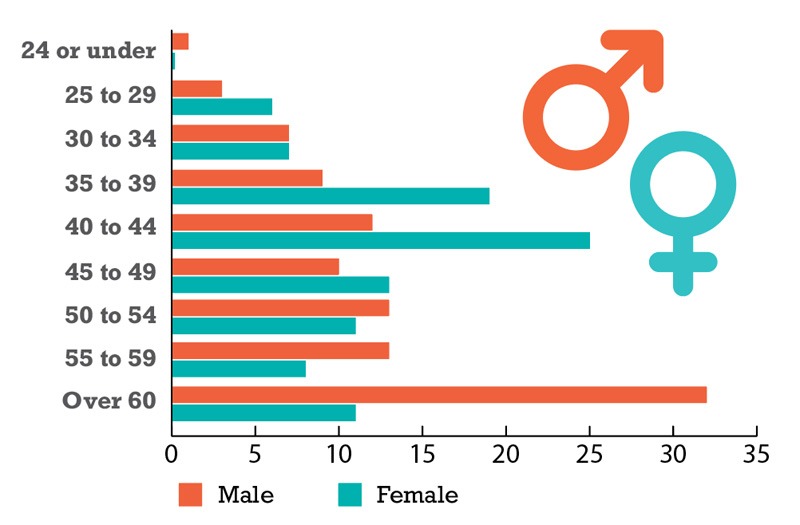

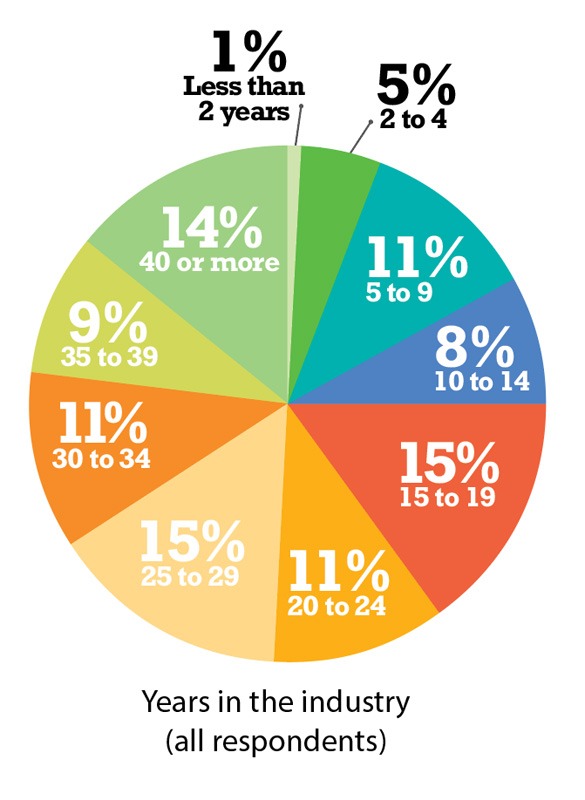

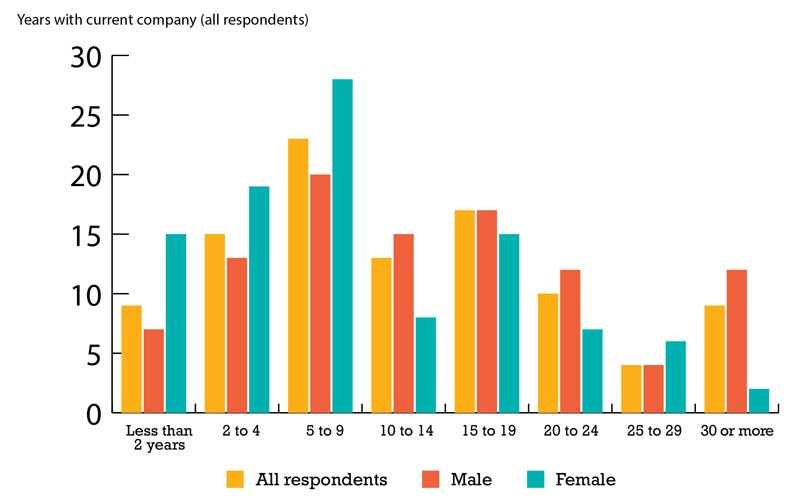

Early-career participation increased, with 24 per cent reporting less than 10 years in the industry. Meanwhile, those with more than 20 years of experience declined slightly, while mid-career representation remained stable.

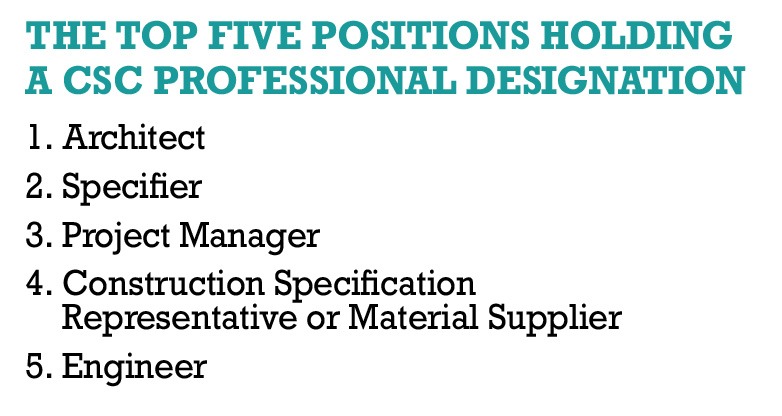

Architects remained the largest group, rising to 32 per cent of respondents. Among them, 44 per cent were women, reflecting a continued shift in representation. Participation among architects increased overall, while other roles, including project managers, specification representatives, material suppliers, and consultants, saw modest declines.

Flexibility fuels work-life satisfaction

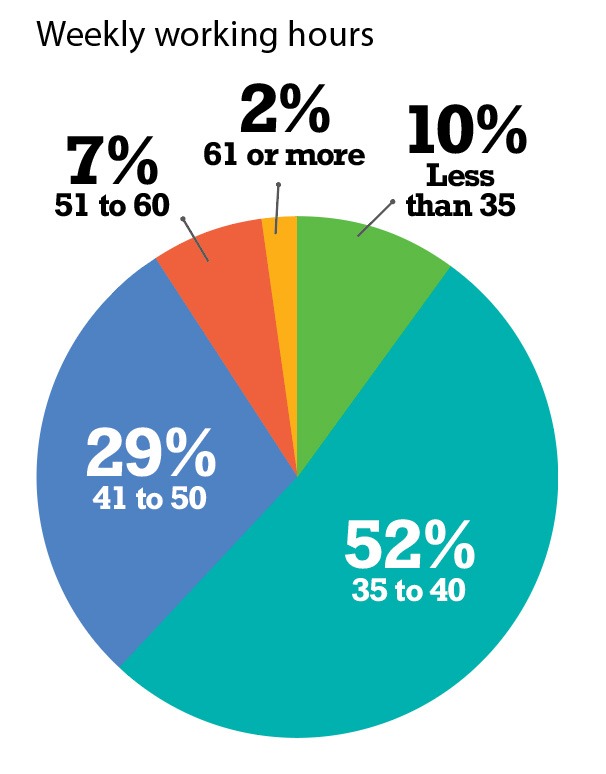

According to Statistics Canada, average weekly hours worked in Canada remained relatively steady through 2025, holding close to the 33.5-hour benchmark reported in late 2024. In this year’s survey, 52 per cent of respondents reported working between 35 and 40 hours per week, aligning with that national figure. Meanwhile, 38 per cent said they regularly work more than 40 hours, a noticeable decline from the previous year. Of those, 29 per cent reported working between 41 and 50 hours, seven per cent between 51 and 60 hours, and two per cent more than 60 hours each week, suggesting a modest easing in extended workweeks across the industry.

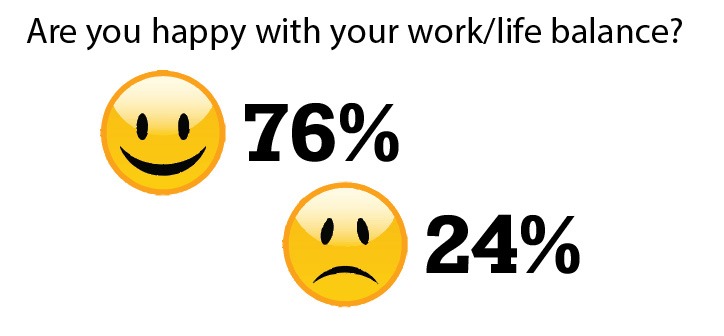

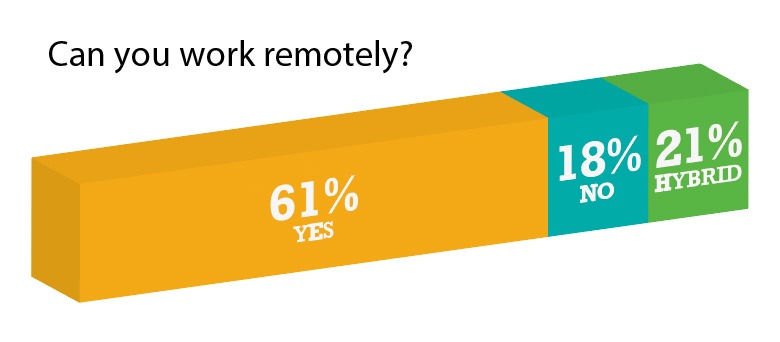

Work-life balance also showed improvement, with 76 per cent of respondents reporting satisfaction. For many, that balance is shaped by flexibility, from remote and hybrid work to greater control over schedules and workloads. “Due to hybrid work, I am able to live where I do and still pursue my hobbies, while visiting family for extended periods,” said one respondent. Another noted, “I work hard, but I choose what I want to work on,” reflecting a broader sense of autonomy shaping how professionals approach their time.

For the 24 per cent who were dissatisfied, however, challenges remain. Sustained workloads, long hours, and competing responsibilities—particularly among firm leaders—continue to weigh heavily. “As an owner, I wear two hats and have to balance project work with business responsibilities,” one respondent shared. Others pointed to limited flexibility, understaffing, and ongoing pressure tied to deadlines, rising costs, and stagnant compensation as key strains on the balance sheet.

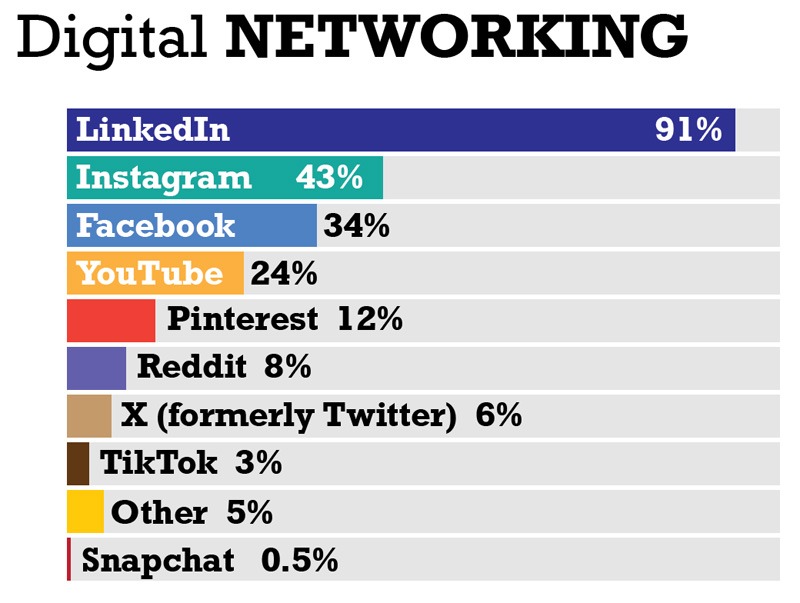

Digital networking

For the seventh year in a row, social media remained part of the professional toolkit for research and networking, though usage declined further to 58 per cent of respondents. LinkedIn continues to lead, used by 91 per cent of those active on social platforms. Instagram saw a notable rise to 43 per cent, while Facebook also climbed to 34 per cent. Elsewhere, activity was more stable, with YouTube and X holding steady, TikTok slipping slightly, and newer additions like Pinterest (12 per cent) and Reddit (eight per cent) beginning to carve out a place in the mix.

While networking still underpins its value, the role of social media continues to evolve. Respondents pointed to its speed and accessibility—a way to quickly scan projects, track industry activity, and discover new ideas. “It’s easier to stay up to date and see what others are working on,” said one respondent, while another noted, “It allows me to connect with people I may not have the chance to meet otherwise and see trends from around the world.” Others emphasized its reach and efficiency, describing it as “a quick way to access information and stay connected with peers.”

At the same time, professionals continue to use social media for visibility, recruitment, and brand building. It offers a way to showcase work, track career movement, and connect with peers and potential hires, particularly as firms compete for talent and seek to expand their reach beyond traditional channels.

Still, not all respondents are convinced of its value. Concerns this year centred less on privacy and more on quality and credibility. Some questioned the depth of the available information, with one noting that social media often presents “a narrow, curated version of reality.”

Others pointed to misinformation and time demands, describing it as “a tremendous waste of time” or expressing further frustration with content that prioritizes appearance over substance.

Taken together, the results suggest a gradual shift from broad adoption toward more selective, purpose-driven use, as professionals weigh the benefits of access and visibility against the need for reliable, high-value information.

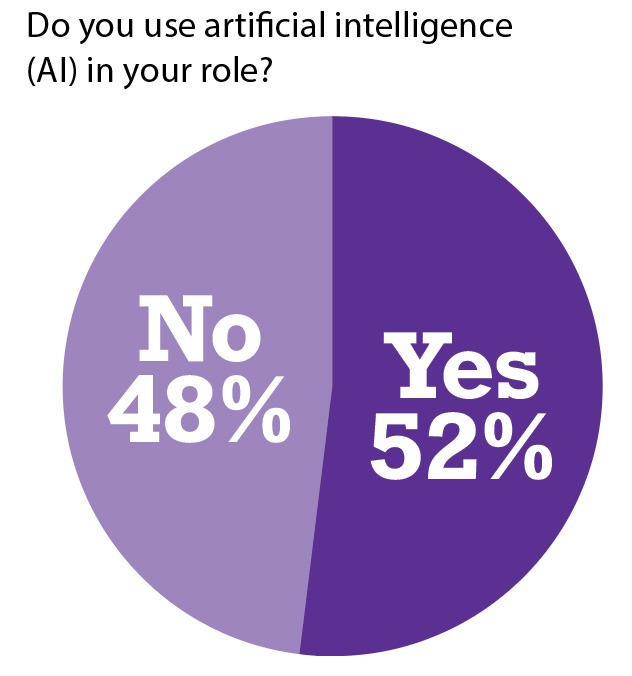

Broader AI adoption: Balancing promise, caution

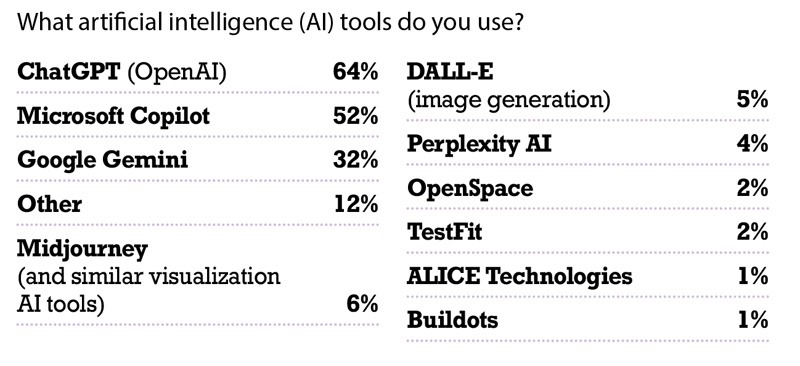

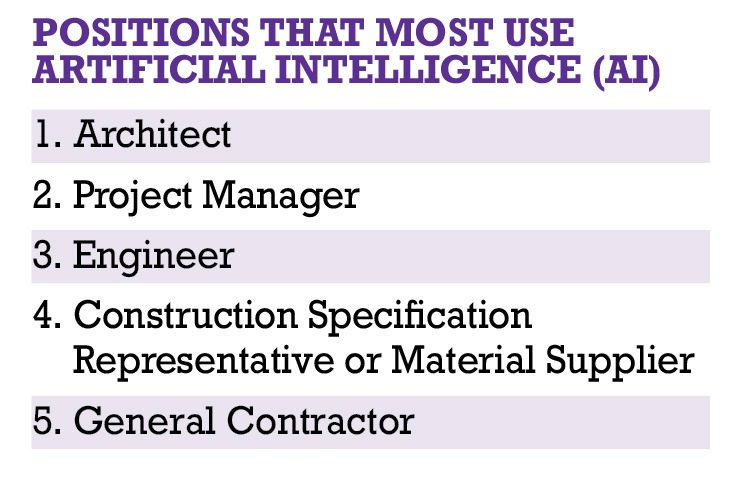

Now in its second year in the survey, artificial intelligence (AI) has moved from early curiosity toward broader, though still measured, adoption. Fifty-two per cent of respondents reported using AI, up significantly from last year. ChatGPT remains the most widely used tool at 64.1 per cent, followed by Microsoft Copilot at 52.3 per cent and Google Gemini at 32.3 per cent. Other tools, including visualization platforms and emerging construction-specific applications, are beginning to gain traction, though at lower levels. Adoption is highest among architects, project managers, engineers, and contractors, while use remains more limited in other roles.

For many, AI’s value lies in efficiency. Respondents pointed to time savings, automation of repetitive tasks, and support for research and documentation. One participant noted its “strong potential to improve efficiency in documentation, co-ordination, and information management.” At the same time, another described it as “a powerful and expedient research tool” for streamlining everyday work.

At the same time, AI is starting to influence how work is approached. Some see it as a “game changer” for design and delivery, while others view it more cautiously, as a tool to support early-stage thinking rather than replace professional judgment.

Concerns remain, particularly around accuracy and oversight. “AI outputs can appear confident but lack project-specific context,” one respondent noted, while others warned of overreliance, skill erosion, and questions around liability and data security.

Taken together, the results suggest AI is following a familiar path, moving beyond experimentation into practical use, but still reliant on human expertise as the industry defines where it truly adds value.

The nature of the business

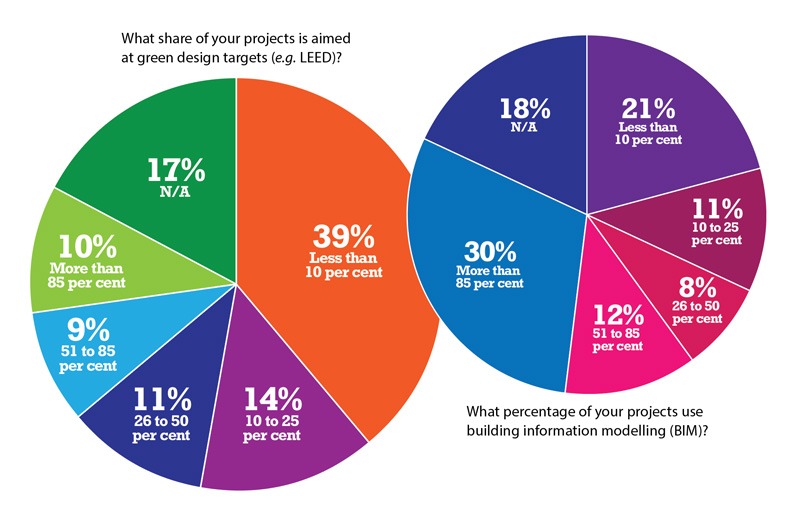

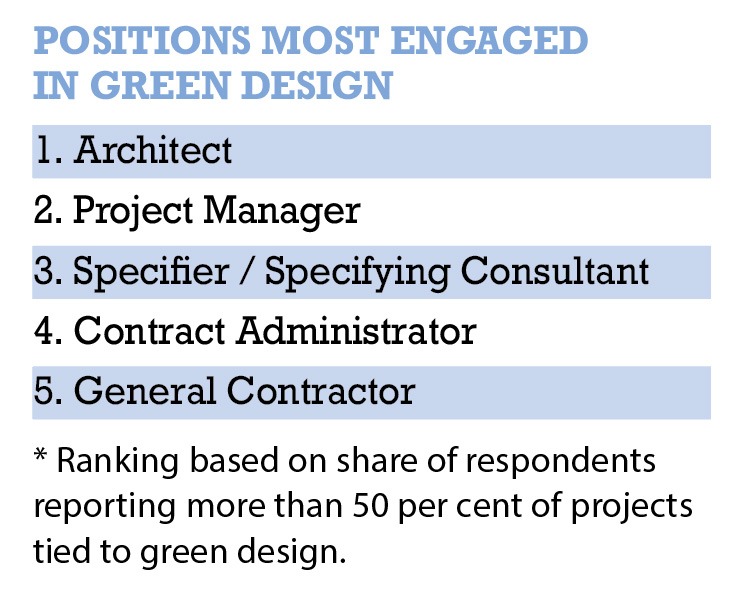

Green targets and BIM

This year’s survey suggests a steadying in the number of professionals deeply involved in sustainable work. Nineteen per cent of respondents reported spending more than half their time on green initiatives, unchanged from the previous year.

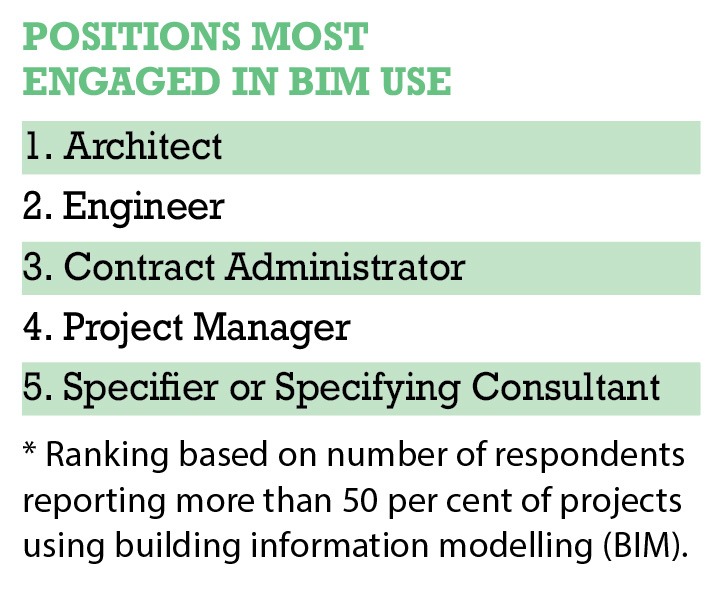

The use of building information modelling (BIM) also appears to be levelling off. Thirty per cent of respondents said they use BIM on more than 85 per cent of their projects, consistent with last year’s results. Even so, many continue to see its potential value. “It is enticing, more productive, enhancing BIM processes and real-time project management,” said one respondent. Others pointed to its broader possibilities, noting that opportunities “are massive and endless,” from improving research and coordination to supporting emerging applications. At the same time, some acknowledged the learning curve, with one participant noting the challenge of keeping pace with evolving tools.

Taken together, the results suggest BIM is entering a more mature phase—less about rapid adoption and more about ongoing refinement, integration, and maximizing value within already established workflows.

Adapting for continued growth

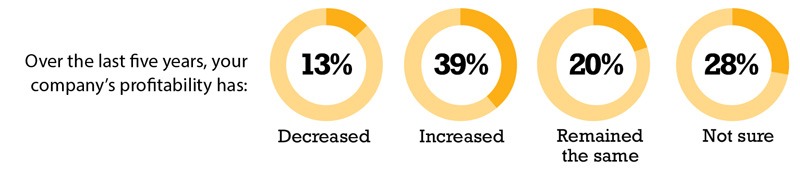

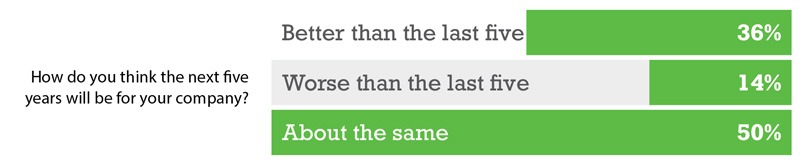

Economic uncertainty continues to shape the industry, though confidence has edged up slightly. Thirty-six per cent of respondents believe the next five years will be better than the last, a modest increase from the previous year. At the same time, profitability showed a slight softening, with 59 per cent reporting their company’s profits have increased or remained stable over the past five years. Meanwhile, the share of those unsure about their firm’s profitability rose slightly to 28 per cent.

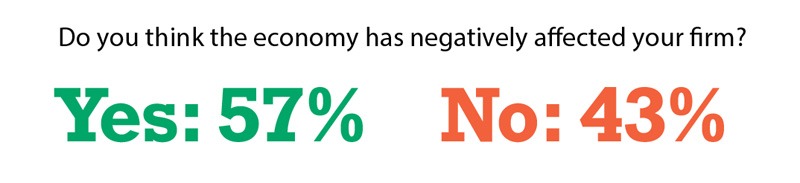

Views on the economy’s impact have shifted more decisively. Fifty-seven per cent of respondents said their firm has felt negative effects, while 43 per cent reported otherwise, signalling a growing concentration of pressure across the industry. A recurring theme in responses was the rising influence of tariffs and trade tensions, now consistently cited as a driver of cost escalation, project delays, and reduced client confidence.

Respondents offered candid insight into these conditions. “Tariffs and shipping costs are having a very real negative effect,” one noted, while another pointed to “projects being stalled and clients becoming more hesitant to spend.” Others described a broader slowdown, with fewer projects advancing and greater uncertainty around pricing and timelines.

At the same time, pockets of resilience remain. “We have continued to grow despite challenges,” one respondent shared, while others pointed to diversification and shifting project types as ways to maintain stability. Still, the outlook remains difficult to forecast. “There are a lot of variables, both in Canada and the U.S., that make it difficult to predict what comes next,” said one participant.

Looking ahead, respondents pointed to a convergence of forces shaping the industry’s trajectory. Economic conditions remain central, but tariffs, geopolitical instability, government policy, labour shortages, and rising costs are increasingly interconnected, compounding their impact on project viability. At the same time, technology is increasingly shaping how firms respond. “Global economic pressure, supply chain volatility, and political decisions are all influencing project viability,” one respondent noted, reflecting the complexity of the current environment.

Taken together, the findings suggest the industry is moving beyond a typical cyclical slowdown into a more structurally constrained environment, where cost pressures, workforce challenges, and policy uncertainty are reshaping how and where work gets done. In this context, the ability to adapt is becoming a defining advantage. As one respondent put it, “Adaptation is the key.”

That adaptability is already taking shape across the industry. Firms are turning to tools like AI to improve efficiency, leaning on BIM to refine co-ordination and delivery, and rethinking how they attract, retain, and develop talent in a tightening labour market. Together, these shifts point to an industry not standing still, but actively recalibrating, balancing near-term pressures with longer-term transformation.

Sign up for our weekly newsletter

Construction Canada weekly newsletters give the latest AEC industry news for those who build, design, engineer, specify, renovate or operate in the built environment.

Products & Services

Read the Latest Issue